The Invisible Score: A Small Business Owner’s Guide to Monitoring and Maintaining Business Credit

- Joy Greenwood

- Apr 29

- 6 min read

Updated: Jul 17

In the quiet, fluorescent-lit corridors of the global financial system, there is a ghost that follows every entrepreneur. It doesn’t sleep, it doesn’t take weekends off, and it never forgets a debt. It isn’t your accountant, and it isn’t the IRS. It is your Business Credit Profile—a digital shadow that speaks about you in rooms you aren’t allowed to enter and influences decisions made by people you will never meet.

Most small business owners treat their business credit like a smoke detector: they ignore it until it starts screaming. They assume that as long as they are "good people" who pay their bills eventually, the system will recognize their integrity. But the world of commercial credit doesn’t care about your integrity. It cares about your data.

COMMON FAQs

Why is business credit sometimes called an “invisible score”?

Because many owners don’t notice it until they apply for vendor terms, financing, insurance, or contracts. Your business credit profile can exist—and change—without obvious day-to-day signals unless you actively monitor it.

What should I monitor regularly in my business credit profile?

Start with identity accuracy (legal name, address, phone, industry), then review reporting trade accounts, payment timeliness, and any public records. Small inconsistencies can create outsized approval issues.

How often should I check my business credit reports?

Monthly is a practical cadence while you’re actively building or correcting a file. Once stable, quarterly check-ins are usually enough—plus an extra check after major changes like an address update or new vendor accounts.

Can errors on a business credit report affect approvals even if I pay on time?

Yes. Incorrect identity data, duplicate files, or misreported payment experiences can trigger denials or extra verification, even when your actual payment behavior is strong.

What’s the difference between monitoring business credit and building business credit?

Monitoring is verifying accuracy and catching changes early. Building is creating reportable payment history through legitimate accounts and consistent on-time (often early) payments. You need both—building without monitoring can allow errors to persist.

What’s a simple first step to maintain business credit health?

Make sure your business identity is consistent everywhere (state filings, bank, website, vendors), then protect payment timeliness with reminders or automation. Consistency + on-time/early payments are foundational signals across bureaus.

In the consumer world, we are coddled by the Fair Credit Reporting Act. We have rights, we have transparency, and we have a scoring system that feels like a high school report card—logical, predictable, and fair. But when you step into the arena of business credit, the safety rails vanish. You are no longer a "consumer"; you are a "commercial entity," and in this world, the rules are written in the blood of high-stakes contracts and the cold logic of algorithmic risk.

If you want to scale—if you want to move from "surviving" to "bankable"—you have to stop treating your credit score as a passive reflection of your past and start treating it as a strategic weapon for your future.

Building business credit is the first step, but maintaining it is an active, strategic process. This guide breaks down the technical mechanics you need to master to ensure your business remains "bankable" and ready for growth.

The Invisible Score: A Small Business Owner’s Guide to Monitoring and Maintaining Business Credit

1. The Reality of the "80 Ceiling"

The most common misconception in business credit is that paying every bill on time will eventually result in a "perfect" score. If you are invoiced on standard terms (such as Net 30) and you pay exactly on or before the due date, your score will be an 80. In the eyes of D&B, an 80 represents "Prompt" payment. While a solid score, an 80 is the functional ceiling for standard trade accounts.

Breaking into the 81–100 Range

To break the 80 ceiling and move into the 81–100 range, your business must be invoiced on discounted (anticipatory) terms and pay within that specific discount window. Examples of these terms include:

2% 10 Net 30: You receive a 2% discount if paid within 10 days; otherwise, the full amount is due in 30.

1% 10 Net 20: A 1% discount if paid within 10 days; otherwise, the full amount is due in 20.

When you pay these invoices within the discount period, the creditor reports the payment as "Anticipated" or "Discounted." This is the only mechanism that triggers a score above 80. If you want a score above 80, you must move beyond "Prompt" and into "Anticipatory" territory.

2. The Mechanics of Dollar-Weighting

The PAYDEX score is not a simple average of your payment history; it is a dollar-weighted calculation. This means that the total dollar amount of each "payment experience" determines how much that specific transaction influences your final 1–100 score.

Why the Size of the Check Matters

In personal credit, a $10 late fee on a credit card can be just as damaging as a $1,000 late payment. In business credit, the scale is the driver.

Weighted Influence: A single $50,000 invoice carries significantly more weight than ten $500 invoices combined.

The Upward Pull: To maximize your score efficiently, you should focus your "anticipatory" efforts on your highest-dollar vendors. Paying a high-value invoice on discounted terms will pull your overall score toward 100 much faster than doing so for a small utility bill.

The Risk of the Large Invoice: Conversely, a late payment on a high-dollar invoice will cause your score to plummet, even if you have dozens of smaller, on-time payments. Your score is essentially a reflection of how you handle your largest financial commitments.

3. The "Silent" Trade Tape Program

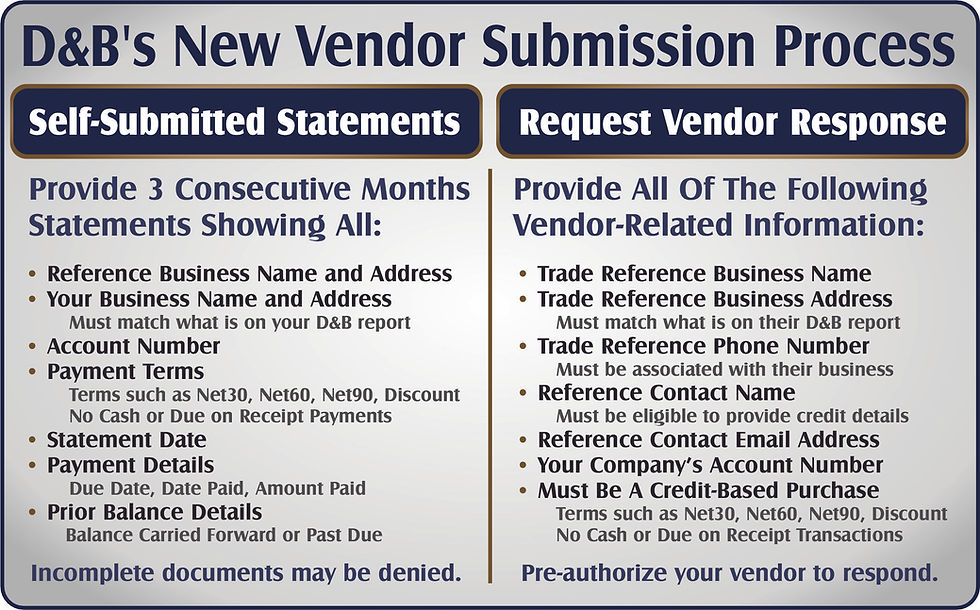

A significant portion of your business credit report is populated automatically through the Trade Tape Program. This is an automated data exchange where large companies (Trade Tape Providers) share their entire accounts receivable ledger with D&B on a monthly basis.

The Confidentiality Clause: One of the most frustrating aspects for business owners is trying to verify which vendors report.

Contractual Silences: Trade Tape Providers are generally prohibited from publicly disclosing that they report to D&B. Disclosing this information is often a violation of their Trade Tape Program contract.

The Myth of the Seal: Many owners look for "D&B Verified" or "D-U-N-S Registered" seals on a vendor’s website as a sign of reporting. This is a mistake. These seals are paid marketing services that any business can purchase; they hold no indication of a vendor’s reporting status or participation in the Trade Tape Program.

Identifying Reporters with D&B Credit Insights: Since you cannot ask a vendor directly if they report, you must monitor your profile using D&B Credit Insights (the service that replaced CreditSignal). By watching your "payment experiences" in Credit Insights, you can see when a new trade line appears. If a new experience populates shortly after a transaction with a specific supplier, you have successfully identified a "silent" reporter.

4. Proactive Maintenance and Auditing

Business credit reports are not infallible. Because reporting is voluntary and comes from thousands of different sources, errors are frequent.

Audit Your Industry Classification: Your North American Industry Classification System (NAICS) or SIC code determines your "peer group." If your business is misclassified into a high-risk industry (like transportation or construction) when you actually operate in a lower-risk field, your "Failure Score" or "Delinquency Score" could be unfairly impacted.

Update Your Identity: Ensure your legal name, address, and years in operation are consistent across all bureaus. Discrepancies can lead to "fragmented" files where your credit history is split across multiple profiles, making your business look less established than it is.

Recency is King: D&B weights payment experiences from the last 12 months more heavily than older data. To maintain a high score, you need a consistent stream of reporting. A score can "go dark" or drop off entirely if your active trade lines stop reporting or the transactions age beyond the 24-28 month timeline.

5. Strategy for the 81–100 Push

If you are currently sitting at an 80 and want to reach the top tier, follow this blueprint:

Identify Your Largest Vendors: List your suppliers by annual spend.

Negotiate Terms: Contact their credit departments and ask if they offer anticipatory/discounted terms (e.g., 2% 10 Net 30).

Execute and Monitor: Pay within that 10-day window and use D&B Credit Insights to verify that the payment is being picked up as "Discounted."

Balance the Weight: Ensure your largest financial obligations are the ones being reported with these favorable terms, as their dollar-weighting will do the heavy lifting for your score.

To keep your enterprise breathing freely, you must master a game of visibility and velocity. Maintaining business credit is easier when you have the right terms, on the right scale, reported through the right channels. By understanding these nuances, you move beyond guesswork. You are no longer just "applying" for credit; you are strategically engineering a profile that commands the best possible terms from lenders and suppliers, ensuring your business never has to gasp for air.

Need help? Just give me a call. Let's review your current business credit profile to see what can be done to help you (and your creditors) breathe a little easier.

Comments