Stop Bootstrapping And Start Building A Business Credit Blueprint

- Joy Greenwood

- Apr 20

- 6 min read

Updated: Jul 17

Let’s be honest: bootstrapping is a badge of honor in the startup world. There’s a certain grit in "doing it all yourself" with nothing but a laptop and a dream. But eventually, that grit can turn into a grind that actually stunts your growth.

Funding your business with personal credit isn't a long-term strategy; it’s a personal liability. If you are constantly dipping into your personal savings or using your own credit cards to fund company equipment, you aren't just building a business—you’re risking your personal life. Dipping into your own pockets isn't "hustle"—it’s a risk you can't afford to take. It’s time to stop surviving on "scrappy" and start building a fundable entity. It's time to stop bootstrapping and start building a business credit blueprint so you can transition from a solo-funder to a credit-worthy powerhouse.

COMMON FAQs

What is a “business credit blueprint”?

A business credit blueprint is a step-by-step plan that aligns your business setup, reporting accounts, and payment behavior so your credit profile builds in a predictable, compliant way—rather than through trial and error.

Why doesn’t bootstrapping always build business credit?

Bootstrapping often relies on cash purchases or personal credit, which may not create reportable business payment history. If accounts don’t report to business bureaus, your file can stay thin even if you’re financially responsible.

What should be in place before opening new vendor or credit accounts?

Your business identity should be consistent everywhere (legal name, address, phone, website/email), and you should have business banking established. Consistency reduces verification issues and helps bureaus match trade lines to the correct file.

Do I need to take on debt to build business credit?

Not necessarily. Many businesses start with vendor terms and small reporting accounts they can pay on time (often early). The goal is documented payment performance—not carrying balances.

How long does it take to see measurable progress using a blueprint approach?

Timelines vary, but many businesses see measurable movement within 60–120 days once reporting accounts are active and payments are consistently on time (or early). Progress depends on reporting cycles and file accuracy.

What’s the most common mistake that slows down business credit-building?

Opening accounts too quickly without confirming reporting and identity alignment. This can lead to denials, duplicate bureau files, or missing trade lines—slowing progress even when you’re doing the “right” things.

Stop betting your personal future on your business’s daily needs. Dipping into your own pockets isn't "hustle"—it’s a risk you don't need to take. When you fund company equipment through personal savings or credit cards, you aren't growing your business—you’re jeopardizing your financial security. Transitioning from a solo-funder to a credit-worthy powerhouse requires moving beyond the "scrappy" bootstrapping phase. Establish a formal business credit blueprint to protect your personal assets and scale with confidence.

Phase 1: Establish Your "Financial Identity"

Incorporate Your Business: Lenders view Sole Proprietorships as "just a person with a job." By forming an LLC, C-Corp, or S-Corp, you create a legal "corporate veil." This signals to banks that the business is a standalone entity capable of entering into its own contracts.

Get Your EIN: The IRS issues this for free. Without it, you’re forced to use your Social Security Number for everything, which ties your business successes (and failures) directly to your personal credit score.

Professional Presence: Creditors use "scrubbing" software to verify your legitimacy. If your business address is a UPS Store or your phone number is just a cell phone, you might be flagged as "high risk." A dedicated business line (even if it is a VOIP service) and a professional domain show you are stable and invested in your business success.

Phase 2: Open the "Right" Accounts

Business Bank Account: This is your primary "evidence" of cash flow. When you eventually apply for a large loan, underwriters will look at your Average Daily Balance. If you’re co-mingling funds with personal rent and groceries, they can’t verify your business's true profitability.

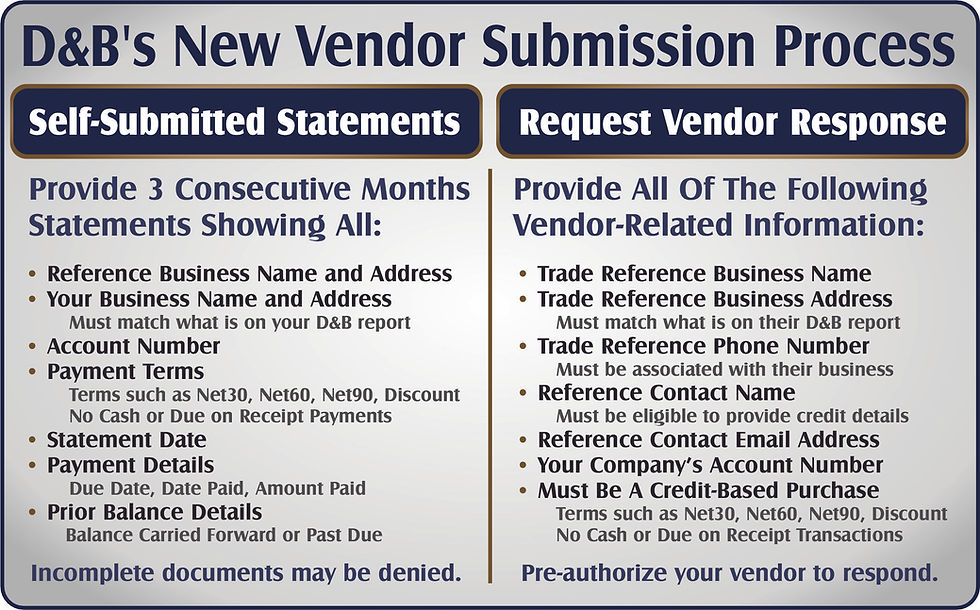

D&B D-U-N-S Number: A D-U-N-S number is a unique nine-digit identifier. Without it, you don't have a Paydex score, which is the standard rating many suppliers use to decide whether to give you terms. While invaluable, the Paydex score is just one of six D&B scores and ratings you need to have in place before you can achieve measurable credit success.

Vendor Trade Lines (Net-30): Most "big" credit cards require a history. You build that history by buying things you already need (toilet paper, printer ink, shipping boxes) from vendors that offer Net-30 terms. You get the items now, pay the bill within 30 days, and they report that positive behavior to the bureaus.

Phase 3: Graduate to Revolving Credit

Store Credit Cards: These act as a "bridge." Because these cards are tied to a specific store (like Lowe's, Office Depot, Staples), the requirements are often lower than a premium bank card. This allows you to build "depth" in your credit report with higher spending limits.

The "No-PG" Goal: A Personal Guarantee (PG) means if the business fails, you are personally liable for the debt. The holy grail of business credit is reaching a point where the business qualifies based on its own merit, protecting your personal house, car, and savings from business setbacks.

Phase 4: Monitor and Maintain

Keep Utilization Low: Just because you have a $50,000 line of credit doesn't mean you should use $49,000 of it. High utilization signals "financial distress" to lenders. Keeping your usage below 30% shows you have access to capital but don't desperately need it.

Pay Early, Not Just On Time: Don't just pay early; seek out vendors that offer early payment discounts. When a vendor reports that you took advantage of a '2% 10 Net 30' discount, it signals to D&B that your cash flow is so strong you can afford to pay early to save money.

Don't obsess over a 100 Paydex: An 80 is the 'optimum' Paydex score, signaling to every major lender that you are a "Prompt" payer who respects contracts. To go higher, you don't need to pay faster; you need different terms. Unless your vendors offer and report "anticipatory" terms like 2% 10 Net 30, your Paydex score will cap at 80 regardless of how many days early you pay.

Review All Scores, Not Just The Paydex: While paying early without discount terms won't impact your Paydex score, it will enhance your overall creditworthiness fitness level by boosting the other five D&B scores and ratings:

• Delinquency Predictor: Predicting the likelihood of severely delinquent payments.

• Financial Stress Score: Predicting the likelihood of business failure.

• Supplier Evaluation Risk: Ranking the business lending risk to suppliers.

• D&B Rating: The company size and overall composite credit appraisal.

• Maximum Credit Recommendation: Highest possible amount suggested for credit lines.

For the purpose of this blog post, framing the 80 as the "optimum score" prevents my readers from chasing a "perfect score" of 100 that is technically out of reach for most, while still positioning those who can "outperform" as a top-tier candidate for lenders.

Check Your Reports Monthly: Business credit bureaus are not regulated by the Fair Credit Reporting Act in the same way personal bureaus are. This means mistakes happen often and can stay there for years unless you proactively dispute them.

The Big Picture

By expanding these points, you’re not just getting a credit card—you’re building fundability. You want to get to the point where a bank sees your business and believes it’s a safe bet to get the funding you need.

The Bottom Line: From Bootstrapping to Building

Building business credit is not a "hack," and it’s no longer about buying office supplies you don't need. In today’s landscape, the bureaus have stripped away the "pay-to-play" shortcuts. To move from a scrappy startup to a credit-ready powerhouse, you must transition from personal liability to corporate fundability.

WARNING: The old "Net-30 Starter Pack" is dead.

Many of the old "legacy vendors" are no longer reporting to the bureaus, have changed their credit account requirements, or have been disqualified from reporting altogether. If you are paying for memberships just to "build credit," you are likely being flagged as a "Cash/COD" account, and that doesn't count toward your company's creditworthiness.

Final Takeaway: Outline Your Strategy

Instead of wasting time on "black-flagged" vendors and ACH auto-drafts that D&B flags as Cash/COD accounts, build a real financial identity by submitting your existing payment history, vendor invoices, bank and credit card statements through Credit Insights Plus, paying your utilities through eCredable or an expense management card, securing a bank-issued credit line, and paying your industrial vendors within the defined terms.

When you build your business credit before you need it, you aren't just getting credit—you’re building an asset that will eventually fund your biggest dreams.

Which of your six D&B metrics is currently dragging down your profile fitness? Just give me a call. Let's review your current business credit profile to see what you can do to graduate out of that bootstrap mentality and design a business credit blueprint that turns your company into a standalone financial warrior.

header.all-comments