Is Your Business "Credit-Ready"?

- Joy Greenwood

- Aug 7, 2024

- 4 min read

Updated: Oct 31, 2025

For many small business owners, one piece of missing or inaccurate information in the business credit report could be the difference between getting the funding you need to grow your company or closing your doors forever. When explaining this to small business owners, I often hold up one of my clients as the perfect example.

CLIENT SPOTLIGHT: Exquisite Property Services

In 2019, I was contacted by Karima Jackson, a young woman who was struggling to build credit for her small New Jersey maintenance company, Exquisite Property Services. Karima was having difficulty understanding the ins and outs of business credit. She'd done a lot of research on the internet and was savvy enough to see that most of the credit-building programs offered online were making wild claims and promoting strategies that employed some pretty risky 'shortcuts'.

"I paid all my bills on time and had a solid income," she says. "However, every time I applied for business lines of credit or attempted to access capital for the company, I was denied. I was frustrated and couldn't figure it out. By the time I reached your website, I didn't know what to believe."

A quick one-on-one walk-thru of her company's D&B report did more than just open her eyes. It opened her mind. And then it opened doors.

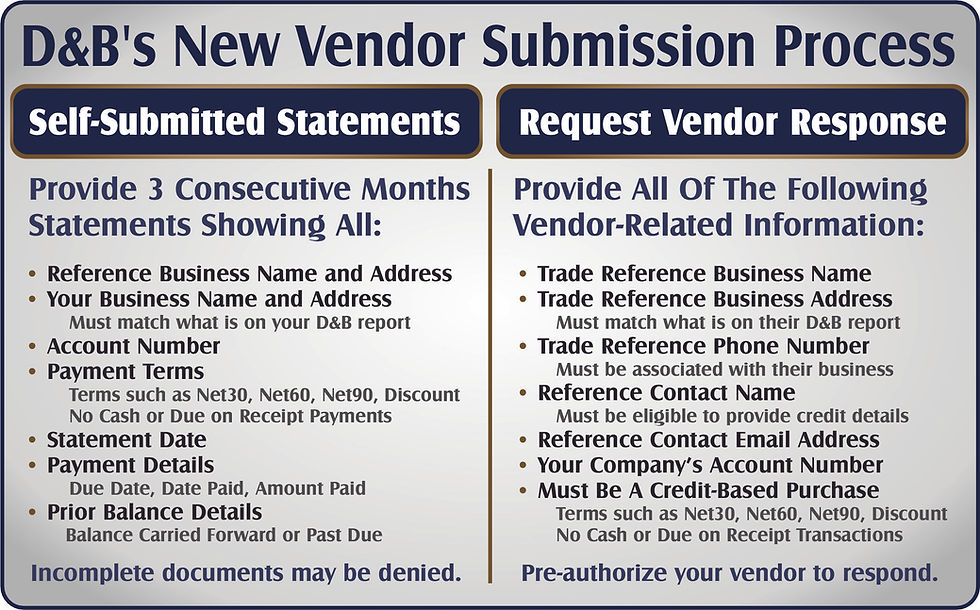

"I just didn't understand the importance of adding accurate NAICS codes," she says. "I didn't realize how much they said about my business, who we are and what we do. Those codes and the other updates we submitted helped to better define the company and validate that we were a legitimate business. Before we made those updates, my company wasn't credit-ready."

In the review she submitted to our Better Business Bureau profile, Karima says, "In 2022, I reached $1M in sales. I've been able to grow my operations and take larger jobs based on the capital I now have access to due to my creditworthiness and due to the strength of my D&B profile."

So I found myself swelling with pride last week. While gathering information about bonding requirements for one of my New Jersey clients, I came across a 2023 story that featured Karima and her business. The story highlighted her participation in a New Jersey Economic Development Authority (NJEDA) small business program that helped her grow her business by teaching her about the bonding process and the part it plays in government contracting opportunities.

As a woman-owned and minority-owned business, Karima admits it hasn't always been easy. "I've made some mistakes and had some hiccups along the way, but that's just part of business ownership — learning along the way and staying motivated."

Over the years, she's taken the necessary classes, participated in programs geared specifically toward helping her small business be more successful, and educated herself about state and local requirements. She's also given back to her community, both voluntarily and as a government contractor. In the process, her company has grown from two 1099 part-time employees to eight full-time staffers, and her fleet of vehicles has grown from one to seven – a source of enormous pride for this small business owner.

But in 2020, while most business owners were facing confusion, thrust headlong into a rapidly devolving pandemic that left many frustrated and hustling for new ways to manage staff, work environments and decreased cash flow, Karima's business thrived. As other businesses struggled to find ways to mitigate the spread of Covid-19, Karima was able to pivot her landscape, maintenance and janitorial business to offer disinfection and sanitation services, something that was suddenly in high demand.

Around that same time, the federal government stepped in with PPP and EIDL loans that, for many business owners, were the difference between staying afloat or drowning in debt. It didn't take long to see that large corporations with well-established credit profiles had no trouble securing federal funding as soon as the programs rolled out, but younger, smaller, local mom and pop businesses weren't so lucky. Many were denied simply because they didn't meet the one qualification requirement for many of these early loans — the same factor that Karima attributes to her company now being "credit-ready" — validation.

For many of those small businesses, the reason for the denial centered around what was (or wasn't) in their D&B business credit report. If the SBA or SBA-approved lenders weren't able to find the company when searching D&B's database, or if they found the company but the information didn't match what was on the company's loan application, they were automatically denied. Because her business was already credit-ready, she was able to secure the funding she needed, and reputable creditors were now approaching her!

In March 2021, Karima and her company earned a major contract with Invest Newark and the Newark Land Bank to provide maintenance and property preparation as part of the group's efforts to revive the city’s abandoned properties. They saw Exquisite Property Services as a trusted partner to meet their needs.

Later that same year, Exquisite was awarded a $1.5 million grant as part of Optimum's celebration of women-owned businesses. That recognition of Karima's hard work and community involvement was deeply deserved.

Throughout Karima's journey, Starpoint has continued to monitor every aspect of her business credit profile for any changes that could have an impact on her ability to succeed.

"My services with Starpoint are an essential part of my business. As long as I am in business, I will continue to utilize Starpoint to monitor, update and advocate for my business' credit health. It's one of the best decisions I have made as a business owner."

But there's a lot more to being credit-ready than just establishing a credit profile or achieving a Paydex score. Potential creditors need to be able to see that your business is legitimate and that you meet all the required criteria. They'll find confidence in seeing consistency in your business details no matter where they look; online, on social media, on state/federal platforms and on all of your business credit profiles.

So, now it's your turn. Is your business credit-ready? If not, give me a call. I may be able to help in ways you can't even imagine!

This story is an inspiring example of perseverance and the importance of understanding business credit. Many small business owners face challenges like Karima did, especially when trying to access funding. Being credit-ready opens doors to new opportunities and can be a game-changer for business growth.

For entrepreneurs who may not have the credit history or established profiles needed for traditional financing, exploring installment loans online can also be a helpful option. These loans provide flexible repayment terms, making it easier for businesses to manage cash flow while working towards building a strong credit profile.