How To Boost Business Credibility

- Joy Greenwood

- Oct 14, 2025

- 6 min read

Updated: Oct 31, 2025

I frequently hear from business owners who face challenges in securing credit approvals despite being profitable and possessing strong business acumen. They believe they have the necessary sharpness, quick insight, and the ability to make sound judgments and prompt decisions. They demonstrate intelligence and seem adept at assessing daily business situations as they occur. They are obviously skilled at analyzing financial data and making profitable decisions. So, what is preventing their progress?

Often, being refused business credit is not at all related to the business owner or even the company's creditworthiness. It's just a matter of knowing how to boost business credibility. While financial statements, bank records, and internal spreadsheets might indicate a prosperous business from an internal perspective, creditors require more than just this data. Anyone can manipulate figures to create an illusion of profitability. However, a creditor's decision will largely hinge on external perceptions — what others say about your business. They need to find confidence in your company's credibility.

STEP ONE: Validating Your Business

Credit underwriters usually begin by confirming fundamental (and frequently overlooked) business information. They examine the company's business registration and annual reports to ensure legitimacy, compliance, principals, operating addresses, duration of service, and other corporate details. This is also where you should start.

Review your business registration in your state's commercial documents portal to verify all information is up-to-date and accurate.

Verify that the business registration is active and in good standing. You may even want to invest a few dollars to purchase a Certificate of Good Standing.

Confirm the physical location, mailing address, principals (if required), registered agent and other pertinent details.

Submit any necessary updates.

If the date for filing your Annual Report is getting close, file it now.

Check the state portal for any liens, suits, judgments or UCC filings. If you find outdated or lapsed filings, see about getting those corrected or removed altogether.

STEP TWO: Review Your Public Presence

I've lost count of how often I've checked a company's website to confirm their business details, only to find outdated addresses or phone numbers, or broken links that don't connect to the correct social media pages. It's crucial for creditors to verify your business information, and the most effective way to ensure this is by maintaining consistency across various platforms. Wherever a creditor searches, the information should consistently point to the same source.

Review every page of your company's website to verify information that is consistent.

Confirm accurate location and contact details are easily available.

Check links to products, services and social media platforms.

Confirm your Privacy and Terms of Use links are current and functioning correctly.

Review your social media links and platforms to make sure they are working and that company details are accurate.

If you haven't posted to your social media sites in a while, now would be a good time.

Perform a basic Google search on your business name, phone number, address, and yes, even your website's domain name to confirm consistent data is being presented.

If your company is registered at the local Chamber of Commerce, Better Business Bureau, trades sites, or other public platforms, verify your company's data is correct.

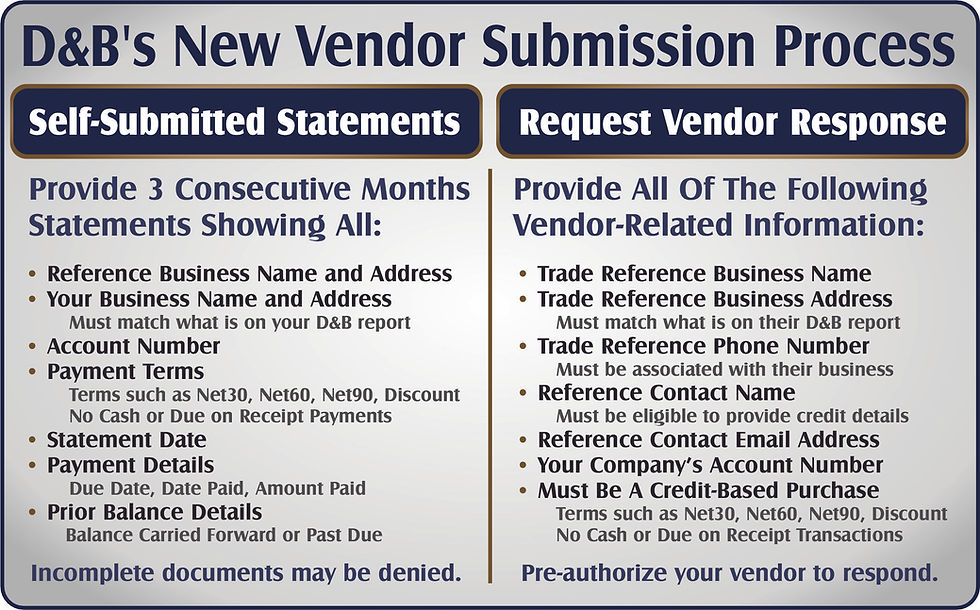

STEP THREE: Update Your Business Credit Reports

Surprisingly, commercial credit bureaus can make errors that might lead to significant financial losses if not promptly corrected. They might have created multiple records for your business at different addresses you've used over time. These records could contain missing or incorrect principal names, street addresses, phone numbers, industry codes, sales figures, and registration details. Additionally, there could be payments, collections, and court records associated with your file that aren't related to your business.

You will need to check Dun & Bradstreet, Business Experian and Equifax Business to ensure the information being presented is accurate.

Dun & Bradstreet provides free access to the data using the DUNS Profile Manager

The business principal can go to my.dnb.com to get free access by verifying their identity and association to the company by either corporate documentation or logging in to the business bank account.

Try to submit all updates at once to reduce time and streamline the process.

Most updates are completed within 72 hours, but they may not be visible in the global database for up to 28 days.

Track changes closely, saving a fresh copy of the report every time there's a change.

Business Experian allows business owners to submit updates to the data for free. Disputing slow payments, collections or public filings requires the purchase of a report in order to identify necessary changes.

A business principal can go to www.businesscreditfacts.com to create an account and get access to the raw company data in the report.

This is a multi-step process that requires identity verification and supporting documentation when necessary.

Some updates will be completed within 24-48 hours, but others could take up to 30 days.

Track changes closely, saving a fresh copy of the report every time there's a change.

The Equifax Business update and dispute process can be a cumbersome and time-consuming one. Take it from someone who knows. I have been trying to correct company data inaccuracies in my Equifax Business report for over six years.

Call the Equifax Commercial department: 800-727-8495

Tell them you need to update your business details and they will start a case.

Provide your business email address

You'll get an email from: commercialdisclosures@equifax.com

Reply to that email with the correct information for your business.

Track changes closely, saving a fresh copy of the report every time there's a change.

STEP FOUR: Prioritize How You Pay Your Business Debt

One of the most common errors small business owners make is in the way they handle bill payments. This isn't about paying bills on time, but rather about ensuring that bills are paid using the company's name and the business's bank account, debit card, or credit card. By maintaining an account under the business's name and creating a transactional history over time, you build historical proof that your business is active and operational, which can facilitate future credit approvals.

Clearly, a crucial aspect of the credit decision-making process will focus on your company's income, stability, longevity, and business credit scores and ratings. Every creditor, lender, or finance agency understands that a history of slow payments to existing creditors could eventually affect them similarly. Currently, we're all facing challenging economic choices. It's understandable that you might need to prioritize which bills are paid on time and which might be delayed. Extending the delay beyond the usual 5-day grace period could jeopardize future credit approvals.

Whenever possible, avoid ACH or automated payments that are automatically deducted from your business bank account. These transactions remove your ability to decide whether to pay or bill early, on time, or late, and they are often reported to commercial credit bureaus as COD or Cash accounts. By choosing to log into your account and make your payment a day or so early, you consciously decide how to repay your debt, which significantly impacts how these transactions are reported to the bureaus.

Did you know that paying your bill on the due date might result in it being reported as a late payment? Many banks, credit card companies, and lenders now use third-party billing and payment processors. When these processors receive your payment, it is marked as received, but it might not be posted to your account until the next day and may not be listed as paid until the payment clears the bank, which could take 1-3 days. By that time, your account might show your bill as overdue. Although the creditor might have measures to prevent charging you a late fee once the payment is processed, the payment date reported to business credit bureaus could be after the actual due date. Making an effort to pay your bills a few days early will help establish a strong history of credibility and creditworthiness.

Generally, by making essential updates, consolidating data, focusing on consistency and clarity, and by prioritizing sound repayment practices, your company's credibility can be significantly enhanced. Consistent, strong data and historical precedent removes doubt and confusion.

If you run into a snag or need any assistance, I'm always ready to help. Simply click here to book a free consultation, or just give me a call at 800-918-7505.

Comments