Disputing Business Slow Payments (And When You May Not Want To)

- Joy Greenwood

- Jul 29, 2025

- 7 min read

Numerous factors can lead to a slow payment being reported on your business credit. These may include temporary financial difficulties, missed due dates, disputed charges, inaccurately reported payment terms, or bookkeeping practices that result in issuing checks too close to a deadline. Every small business owner is likely to encounter situations where their business credit report is adversely affected by one or more slow payments.

Typically, the initial reaction is to contact the commercial credit bureau to report misconduct or threaten legal action. I am well-acquainted with this scenario. Fifteen years ago, as an escalation and resolution specialist at Dun and Bradstreet (and subsequently at Dun & Bradstreet Credibility Corp), I was responsible for diplomatically managing irate callers who threatened retaliatory measures. Known as "walking the caller off a ledge," I would calmly explain how and why slow payments were in the credit report, offer options to remove the disputed transaction, and, if necessary, guide the customer through the dispute process. My job security was dependent on whether the call ended without further escalation.

COMMOM FAQS

What is a “slow payment” on a business credit report?

A slow payment is an invoice reported as paid after the agreed terms (for example, net-30 paid in 45 days). Business bureaus use these payment experiences to help assess risk.

Why do slow payments show up even when a business is generally responsible?

They can result from temporary cash-flow issues, missed due dates, disputed charges, bookkeeping timing (like mailing checks too close to the deadline), or reporting errors such as incorrect terms or dates.

What are the main ways payment history gets added to a business credit report?

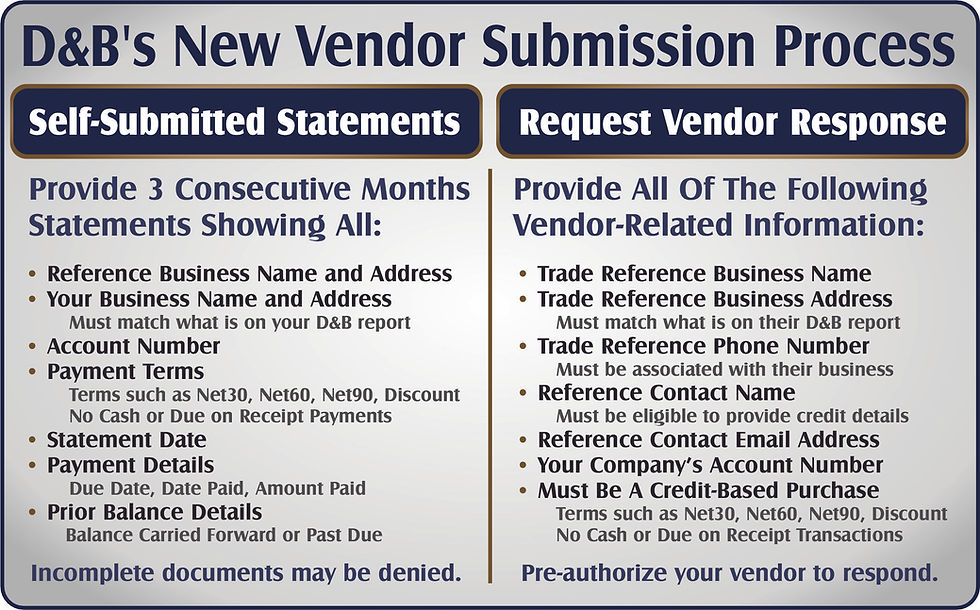

Payment history is typically added through (1) vendor/creditor auto-reporting, (2) bureau-initiated research or linkage to other data sources, or (3) customer-initiated submissions where the business requests that payment experiences be added or verified.

When should I dispute a slow payment—and when might I avoid disputing it?

Dispute when the entry is inaccurate or incomplete and you have documentation to support a correction. You may avoid disputing if the item is about to age off the report, because a dispute can sometimes cause the bureau to re-verify and refresh the reporting date.

What documentation helps support a slow payment dispute?

Invoices showing terms, proof of payment, payment posting dates, and any written vendor confirmations. The goal is to clearly show the correct timeline and terms so the bureau can validate the correction.

What’s a practical strategy if a slow payment is accurate but hurting my scores?

If the vendor is still active, one approach is to re-use the vendor and pay early/on time so a new positive payment experience is reported. Over time, strong recent payment behavior can reduce the impact of older negative entries.

The How and Why of Payment History

There are three methods by which payments, whether favorable or unfavorable, are incorporated into a business credit report. The approach for disputing slow payments will depend on the method by which the payment was originally recorded in the report.

GENERIC — Auto-reporting by vendors, suppliers and creditors

• Banks, credit cards and municipalities

• Financial lenders and third-party agencies

• Vendors, suppliers and payment processors

FORCED — Internal transaction research by the bureau itself

• Archived payment history

• Linkage to business bank accounts

OPTIONAL — Customer-initiated adding of payment history

• Manual submission of vendors and suppliers

• New accounts with auto-reporting vendors

• Company updates that spur payment research

Options For Removing Offending Transactions

When a derogatory transaction appears on a business credit report, there are multiple strategies available for addressing it. These include options for removing the transaction, converting it from a negative to a positive payment record, or allowing it to naturally expire from the report. You'll want to start by determining whether or not you want to dispute the slow payment.

Below is an example of a slow payment that is being actively reported.

I typically suggest that this type of transaction gets converted to a positive. The easiest way is by disputing the transaction, but then re-using the vendor again and paying the invoice on time. You will not only benefit from the removal of the slow payment, but your scores will earn a boost when the vendor reports your most recent purchase as a positive transaction.

YOUR STEPS:

• Dispute the slow payment to see if it can be removed from the report

• Re-using the vendor for a new purchase.

• Be sure to pay the invoice well before the due date.

Below is an example of a slow payment that was reported several months ago.

I typically suggest that this type of transaction gets disputed. It has been over a year since the vendor last reported the negative experience, and it is not being re-reported on a monthly basis. If your slow payment dispute is successful, the payment will be removed and your scores will see an improvement.

YOUR STEPS:

• Dispute the slow payment to see if it can be permanently removed

• If removed, watch for a boost to your scores.

• If not removed, contact the vendor to see if they will correct the record.

• You may want to re-use the vendor to get new positive payments added.

Below is an example of a slow payment that is about to drop off the report due to its age.

I typically suggest that this type of transaction is allowed to drop off on its own. Payment history only stays on the credit report for 24-28 months. If you dispute this slow payment, it may get verified as accurate and added back into the report with a more current date. That would restart the two year clock again. If you allow it to drop off the report completely, there is no chance it will return to the report at a later date.

YOUR STEPS:

• Do nothing.

• Allow the slow payment to drop off the report.

• Watch for a boost to your scores and ratings.

Disputing Business Slow Payments

Step One: Access the business credit report

• Dun and Bradstreet provides free access to the business credit report via the D-U-N-S Manager. You can register for access at www.dnb.com.

• Business Experian provides free access to the business credit report via their Smart Business Reports portal. You can register for access at www.smartbusinessreports.com

• Equifax Commercial's process for changes and disputes is more complicated and time consuming. You can request access by calling their commercial division at 800-727-8495.

(In depth dispute instructions for each commercial bureau are listed below.)

Step Two: Save a copy of the existing payment history

Be sure to save a copy of your credit report every time you check for changes. This will not only assist you in documenting changes as they happen but may also enable you to identify which companies are reporting and re-reporting payments to the business credit bureaus.

Step Three: Launching the slow payment dispute

DUN AND BRADSTREET

In D&B's D-U-N-S Manager, you have the capability to initiate a dispute concurrently with updating your business details. Often, a simple data update can enhance credit scores and ratings. Additionally, removing a slow payment can provide further improvement. On the Payments tab, locate the derogatory transaction you wish to dispute and select the appropriate reason from the dropdown menu on the right. Proceed to review and submit the updates and disputes.

Hint: This portal times out pretty quickly. If it does, you'll need to repeat the process again.

Timeline: Most disputes are resolved with 10-14 days.

BUSINESS EXPERIAN

To update or dispute information with Business Experian, submit your requests via email. After accessing your report, print it and mark the sections requiring correction. Clearly circle the items in question, provide a concise explanation of the inaccuracies, supply the correct information, and attach supporting documentation if available. Compile these documents into a single PDF file and email it to: BusinessDisputes@experian.com

Hint: To avoid unnecessary delays, try to submit all updates and disputes at the same time.

Timeline: Most disputes are resolved within 30-60 days.

EQUIFAX COMMERCIAL

Please contact the Equifax Commercial department at 800-727-8495 to update your business information. Provide your company name and email address to initiate a case. You will receive an email from commercialdisclosures@equifax.com. Respond to this email with your full name and company name. They will then send you a copy of your credit report. If there are any derogatory payments, mark them for dispute and include a separate page detailing the necessary changes. You may fax the changes to 888-826-0711 or email them to: cust.serv@equifax.com

Hint: It's very difficult to successfully accomplish disputes and changes with Equifax.

Timeline: Disputes can take 6 months or more, and some updates may never be completed.

Step Four: Track all updates to the reports

It is essential to diligently monitor any modifications to your business credit reports. Watch your email inbox for confirmation that your change request has been received. Set a reminder in your digital calendar to review your business credit reports at least every two weeks. Print and save a copy of the report each time you check for updates. Compare the reports and document all changes as they occur. If no updates or changes are visible within 30 days, resubmit the request for a second attempt. Should there be no changes within 60 days, I recommend that you contact the bureau directly.

Step Five: Stay on top of your report

Once your updates and disputes are completed, set a reminder on your digital calendar to ensure you review the report monthly. By actively engaging in this process, you reduce the likelihood of unforeseen impacts on your scores and ratings down the road.

Step Six: Ask for help if you need it

Starpoint Credit Solutions offers complimentary advice and strategies on our website to enhance your business credit scores and ratings. Additionally, we offer paid services to assist with implementing updates, resolving payment disputes, and monitoring changes in your business credit reports on a daily basis. If we identify areas for improvement, we guide you through the necessary steps to address them effectively. Once your credit report is optimized, we can recommend tailored funding options to suit your company's requirements.

Please feel free to reach out to me directly at 800-918-7505 if you have any questions, if you would like a one-on-one business credit review, or if you need immediate assistance.

Comments