Business Credit: One-Size-Doesn't-Fit-All

- Joy Greenwood

- Jul 18, 2024

- 4 min read

Building business credit is a lot like shopping for blue jeans. No two people's bodies, preferences or needs are exactly alike, and neither are their businesses. Even individual branch locations of the same company are going to have different expenses depending on their location, staff, size and their particular costs of operating on a day-to-day basis.

So why would anyone think the exact same vendors, suppliers, products and services are going to fit each individual business the same way? Because a cookie-cutter, one-size-fits-all strategy is easy. It allows them to run more clients through their process faster, regardless of what those companies need, or where they end up. They see their customer's businesses as a statistic rather than focusing on what your business actually needs to get to your end goals.

Business Credit: One-Size-Doesn't-Fit-All

One-size-fits-all creditbuilding is what's easiest and most profitable for their business, not yours. They prefer it because it requires no independent thought from their staff! Everything is "Copy and Paste" or "Steps 1-4" or "Tiers". At Starpoint, we do things differently. We customize our business around your business credit needs.

COMMOM FAQS

Why doesn’t a “one-size-fits-all” vendor list work for business credit?

Because every business has different expenses, cash flow, industry needs, and risk factors. Using the same vendors as everyone else can create patterns that don’t reflect your real operations—and may raise credibility concerns.

Can using the same tradelines as other businesses hurt my credibility?

It can. When many unrelated businesses show identical vendor patterns, it may look manufactured rather than organic. Bureaus and underwriters often prefer to see payment history that matches your actual business activity.

What do business credit bureaus look for besides scores?

They look for consistency and legitimacy signals: accurate business identity details, a believable mix of vendors, stable payment behavior, and reporting that aligns with your industry and operations.

What’s a safer alternative to cookie-cutter credit-building?

Build credit around what your business truly uses: add/verify your existing payment history where possible, then supplement with a small number of reporting vendors that fit your operations and you can pay on time (often early).

Why is adding existing payment history often faster than opening new tradelines?

Because it leverages transactions you’ve already made. When eligible payments can be verified and reported, you may strengthen your profile without waiting months to “season” brand-new accounts.

How do I know which vendors are the right fit for my business credit goals?

Start with your end goal (vendor terms, cards, loans, contracts), then match vendors to your industry, spending patterns, and reporting needs. The right mix is the one you can use consistently and pay reliably—without forcing purchases that don’t fit your business.

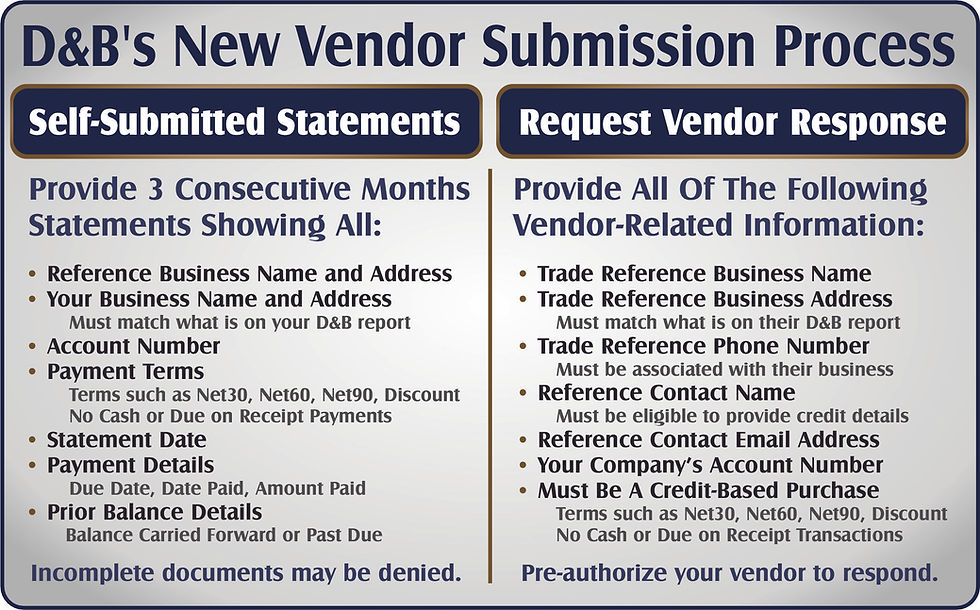

In reality, business credit bureaus like D&B have made it a part of their practice to track those one-size-fits-all patterns of suspicious behavior and the run-of-the-mill tactics that come and go like the seasons. If the only vendors and suppliers (tradelines) that you have are the same ones the guy next door has, and the guy next door to him has, you've just put yourself (and your business credit) at risk... and that's NEVER a good thing!

Companies who sell a one-size-fits-all strategy to their clients don't care about their client's companies. They are only focused on their own bottom line. Their cookie-cutter technique will do more harm than good because it sends a message to the bureaus that your business is only as credible as the thousands of others who have used those same techniques. Credit card issuers and bank underwriters recognize those techniques, too. They learned the hard way that many of the companies that used them have turned out to be high-risk, fraudulent entities who ran out on their debts.

If your business is legitimate, it deserves to be seen and judged on its own merit. For your potential creditors to find value and credibility in your credit history, they need to see a variety of vendors and suppliers that are geared specifically toward your company, your industry, your financial activity, your location, your size, your needs, and your capability to engage vendors, make purchases and pay bills on time.

Nine times out of ten, adding your own existing payment history to your business credit report is going to be far more beneficial than following someone else's cookie-cutter roadmap. If you've already been paying bills and making purchases in your day-to-day operations, those transactions are the ones that are going to say more about your company's capability and credibility than any cookie-cutter tradelines ever could.

Not only is adding your own existing payment history faster and more reliable, it's also a lot more cost effective because those transactions represent money you've already spent. Adding your existing payment history to your business credit profile allows your company to ... well ... get "credit" for what you've already paid!

If you've struggled to build business credit or fallen into the one-size-fits-all trap and would like to move beyond those risky strategies, just give me a call.

I'm here to help — 800-918-7505.

Comments